- 27

- Jun

One of the worst things borrowers overlook when comparing lenders can also be one of the biggest mistakes they can make. Investors, even experienced ones, can be tempted by too-good-to-be-true interest rates or no-money down loans. These are great on their own, as long as the lender’s goals are the same as yours. What we are seeing more and more of in this business are what we refer to as ‘Loan-to-own’ shops – where the primary goal of the lender is to take back your property – and your equity becomes their profit.

When you are shopping for a lender, one of the best questions you can ask is “What is your foreclosure rate?” This simple question can tell you a lot about a hard money lender. If they won’t answer, you have a lender who isn’t being transparent. Foreclosures happen to good people, but a good lender will do their best to keep it from happening in the first place. Whether that means facilitating work-out solutions or loan modifications, most lenders don’t want to take a property back.

If a lender has a high foreclosure rate, you can be sure that they are writing loans that are at higher risk in the first place. They put their borrowers into loans that they know will be hard to get themselves out of, either because the monthly payments were more than they could ever afford or because the project was more than they could handle This is where the loan-to-own lenders operate. They write loans that they not only hope will default, but they can even be active in pushing the property to foreclosure.

Being in this business, we’ve had the unfortunate experience of having to deal with these types of lenders more than a few times. In one such instance, we were helping a borrower refinance another lender’s hard money loan. The only problem was he needed to do it quickly as his loan was about to mature. The title company spent weeks trying to get a payoff statement from the lender, only to receive it the afternoon before the loan matured. The payoff statement was riddled with errors that amounted to thousands of dollars in additional fees and the lender then warned the borrower that they were starting foreclosure proceedings the following day if the loan wasn’t paid in full. The borrower was forced to file a Temporary Restraining Order against the lender so they couldn’t file a foreclosure notice while they sorted out the payoff.

Most lenders make the bulk of their revenues from monthly interest payments. If they have to foreclose on a borrower, those monthly payments stop and the lender stops making any money from the loan. For your average lender, this is a very bad thing. If the prospective lender has a low foreclosure rate, you can be sure that they are writing more conservative loans that help keep them (and their borrowers) out of trouble. Also, this is a great indication of how a lender will work with you if everything doesn’t go exactly to plan – which it never does. If your lender’s goal is to make revenue off the monthly payments until you are able to pay the loan back, it is in their best interest to work with you on extensions, draw schedules, refinances, etc., if you ever need that. The lender who is trying to get your property from you does not want to help you out!

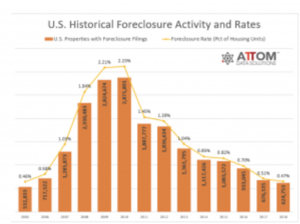

So what is a decent foreclosure rate? To give you a point of comparison, the national average for primary home loans in 2018 was 0.47%. Eight years previous at the height of the Mortgage Crisis, the rate was 2.23%. (As an aside, Corridor Funding’s all time foreclosure rate is 0.3% – meaning that for every 1,000 loans we write, we are forced to foreclose on three. That’s lower than the national average for people paying to keep a roof over their own head!). Some lenders in this space have foreclosure rates of 10-20%! These are the lenders to watch out for! The next time you see an offer for a 100% Loan-to-cost loan or zero interest for the first 60 days – run the other way and find a lender that will be around to help you finance your deals for the long-haul, like Corridor Funding.